Search Site

1790 Hughes Landing Boulevard, Suite 200 | The Woodlands, Texas 77380

*Commitment Free Inquiry

281-367-1222

Typically when one considers buying a foreclosed property, they envision purchasing a property at a foreclosure sale on the courthouse steps. While thousands of properties are sold each month at such foreclosure sales, many of the foreclosed properties are purchased at these foreclosure sales by the bank holding the mortgage. Banks typically will not hold real estate long term as a bank’s ability to own real estate is heavily regulated. Accordingly and in an attempt to recoup their cost associated with the foreclosure, the bank will place the property on the market for sale.

Locating Foreclosed Properties

Foreclosed properties are typically listed for sale in the same manner as non-foreclosure properties. There are many brokers that specialize in foreclosed or “bank-owned” properties and these properties are listed on the Multiple Listing Service (MLS). Locally, properties in the greater Houston Area (including most parts of Montgomery County) are listed on the Houston Association of Realtors’ website www.HAR.com. In addition to being listed on an MLS, a bank may also list foreclosed properties that it owns on its website.

The Purchase Process

The process of purchasing a foreclosed property from the bank is similar to purchasing a non-foreclosed property with the exception that the seller of the property is the bank. While the foreclosure process will serve to clear the original mortgage and most ancillary liens, it is important that the buyer conduct adequate due diligence to ensure that the title to the property is clear and that there are not outstanding encumbrances on the property that are not satisfied at closing. It is also equally important that you have the property inspected by a licensed inspector to ensure that there are no unknown defects or problems with the property.

Risks of Purchasing Foreclosure Properties

The potential risks of purchasing properties at a foreclosure sale (namely little or no time to fully inspect the property and conduct an exhaustive title and lien search) can be substantially minimized when purchasing a bank-owned property as long as the buyer obtains and utilizes proper professional services. The bank will often have the utilities turned off on a property to save expenses, so a complete inspection of the property may be hampered or limited. Because the bank attempts to minimize their expenditures on the foreclosure properties, the properties normally sold “as-is” and the bank is typically not willing to make repairs or improvements to the property.

Eric R. Thiergood, Sr.

Phone: 281-367-1222

Fax: 281-210-1361

Contact a Dedicated Texas Business Lawyer To Schedule a Consultation

Call 281-367-1222 or contact us online to schedule a meeting.

Recent Blog Posts

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

By The Strong Firm P.C. / March 13, 2024

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

As trusted legal advisors, we understand the complexities and challenges that employers face when navigating the landscape of employment law. With the ever-evolving regulatory environment, it's crucial for employers to stay informed and proactive in addressing legal concerns.

One

Read More

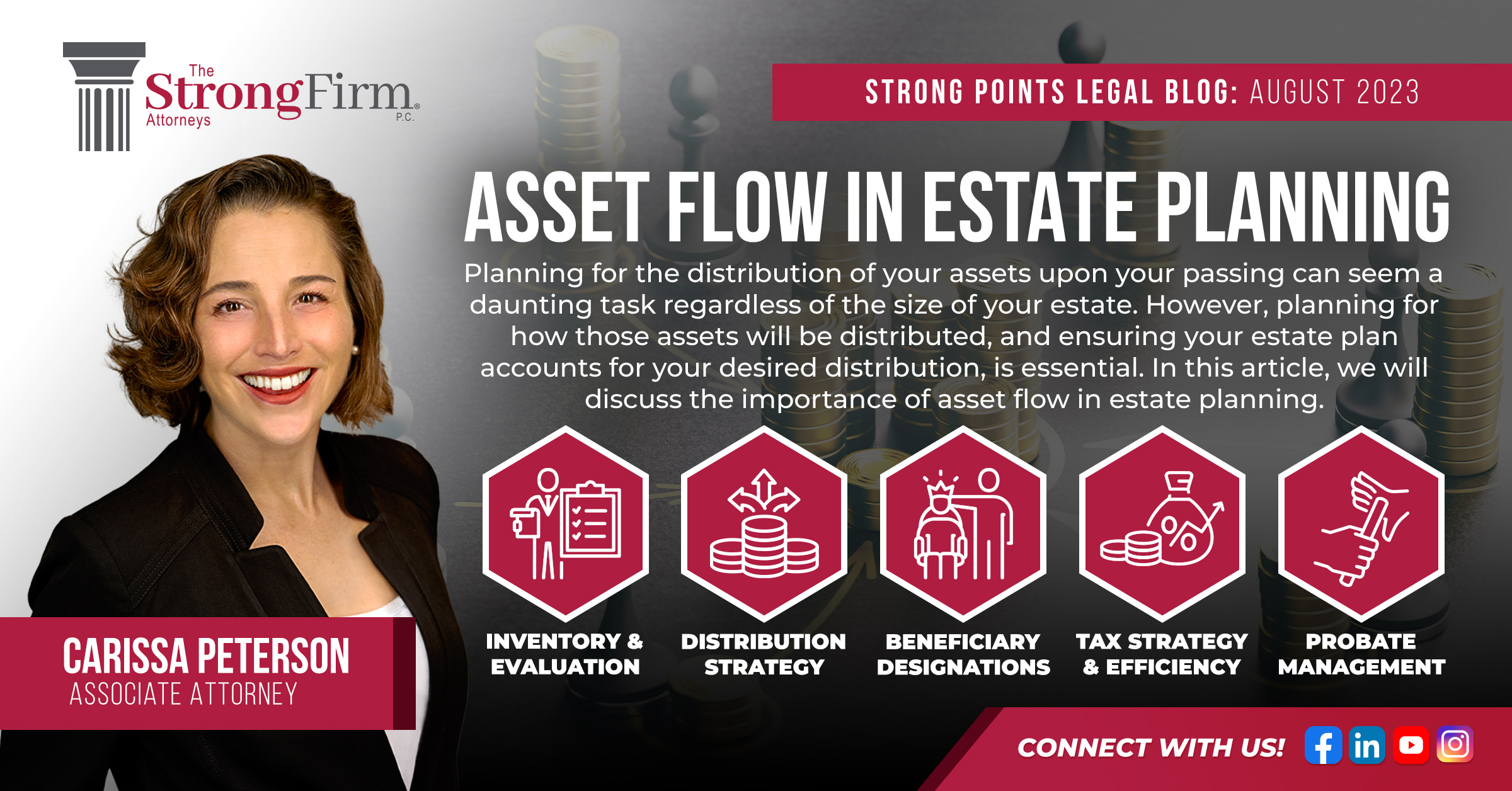

Asset Flow in Estate Planning

By Carissa Peterson / August 21, 2023

Planning for the distribution of your assets upon your passing can seem a daunting task regardless of the size of your estate. However, planning for how those assets will be distributed, and ensuring your estate plan accounts for your desired distribution, is essential. In this article, we will discuss the

Read More

Kelly Sullivan Joins The Strong Firm P.C. As Senior Counsel

By Bret L. Strong / June 10, 2022

The Strong Firm P.C. is excited to announce the addition of Kelly Sullivan to its team of experienced attorneys. Kelly adds exceptional strength to the firm’s established practice areas based on her wealth of experience in the areas of Litigation, Labor and Employment Law, Business Law and Governmental Law, Zoning

Read More

The Future of Non-Compete Agreements: Executive Order on Promoting Competition in the American Agreement

By Kristina Frankel / April 22, 2022

In July 2021, President Biden signed an Executive Order aiming to limit the use of restrictive covenants in employment relationships. Opening with the premise that “a fair, open, and competitive marketplace has long been a cornerstone of the American economy, while excessive market concentration threatens basic economic liberties, democratic accountability,

Read More

-

Video Vault

Watch videos done by our legal team to gain a better understanding of your legal needs. Our lawyers give video insight into areas such as Real Estate, Business Law, Mergers & Acquisitions and much more.![]()

Contact us