Search Site

1790 Hughes Landing Boulevard, Suite 200 | The Woodlands, Texas 77380

*Commitment Free Inquiry

281-367-1222

With the increase of software packages and online companies that provide forms to complete your estate planning many people think their wills or trusts should be “one size fits all.” Unfortunately, there are very few things in the law that apply equally well to all people and all circumstances and estate planning is no exception. Instead, it is important to be thoughtful about your approach to estate planning because—if for no other reason—you will no longer be around to clear up any misunderstandings or difficulties created by poorly crafted documents.

In 2013, the American Taxpayer Relief Act (“ATRA”) was signed into law allowing US citizens to give up to $5.0m dollars ($5.45m[1] in 2016 after being indexed for inflation), at the time of their death without any estate taxes being owed. This marked a significant increase from the $1m dollar exemption that would apply if the ATRA was not passed and marked a change in estate planning for the majority of clients. First, the exemption amount meant that a much smaller percentage of clients needed to engage in estate tax planning. Second, changes in the rates for capital gains taxes placed estate tax planning at odds with long-term income tax planning. The result: We frequently see client with estate plans that are more complex than is warranted by their circumstances, giving plans and/or assets levels.

As alluded to above, overly complex planning to deal with estate taxes may have a negative impact on the amount of income taxes that are ultimately paid on the property you leave behind. Possibly more important, overly complex planning tends to lead to more expensive and complex legal issues when administrating your plan. The various trusts and entities that were conceived in a time when the estate tax exemption was much lower, your asset level was higher and/or your circumstances were more complex may no longer be applicable. Accordingly, it is important to remain vigilant regarding the size and complexity of your estate plan and tailor those plans to the law and your circumstances as they exist now.

[1] https://www.irs.gov/Businesses/Small-Businesses-&-Self-Employed/Whats-New-Estate-and-Gift-Tax

Royce Lanning

Phone: 281-367-1222

Fax: 281-210-1361

Contact a Dedicated Texas Business Lawyer To Schedule a Consultation

Call 281-367-1222 or contact us online to schedule a meeting.

Recent Blog Posts

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

By The Strong Firm P.C. / March 13, 2024

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

As trusted legal advisors, we understand the complexities and challenges that employers face when navigating the landscape of employment law. With the ever-evolving regulatory environment, it's crucial for employers to stay informed and proactive in addressing legal concerns.

One

Read More

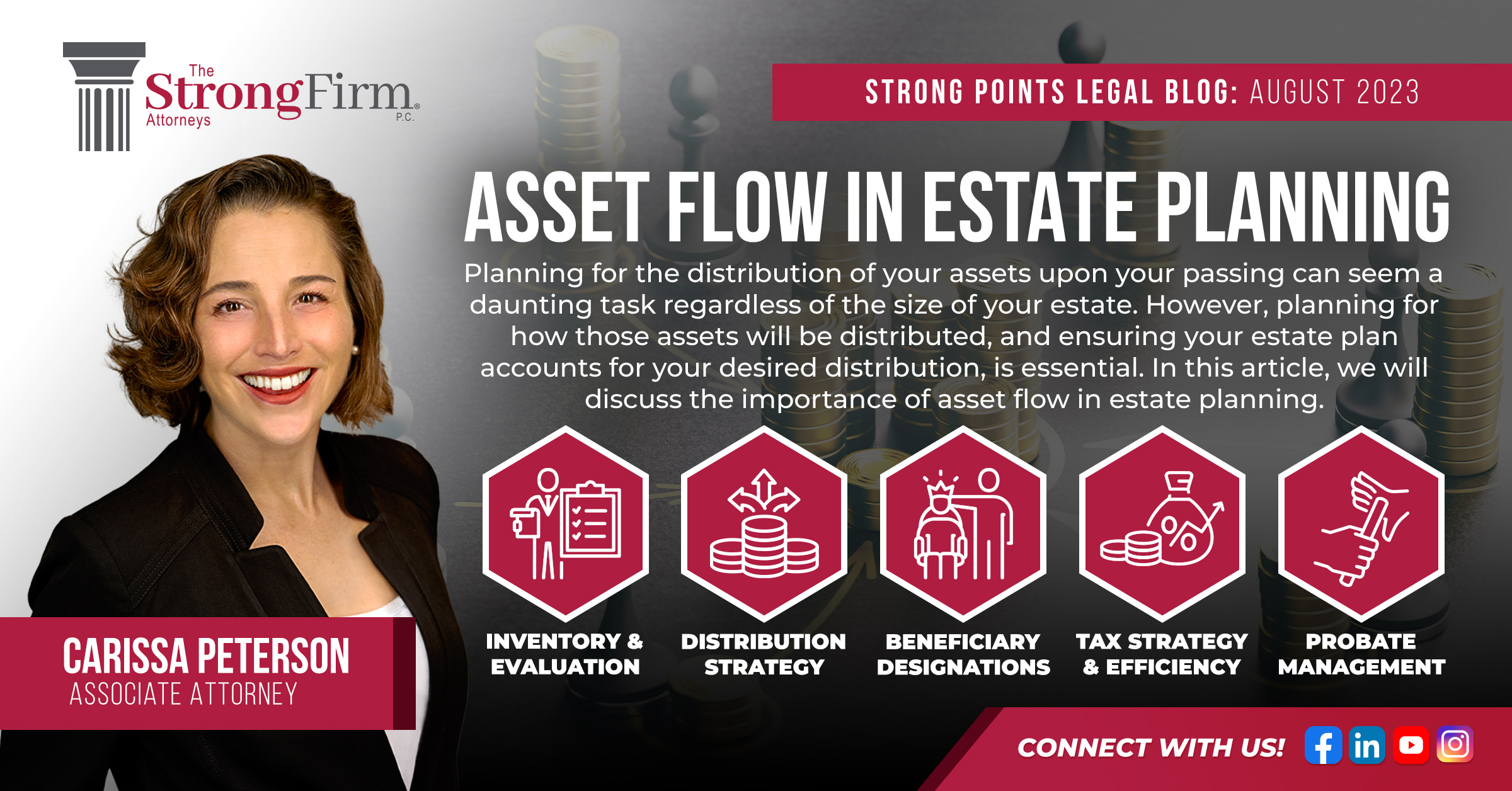

Asset Flow in Estate Planning

By Carissa Peterson / August 21, 2023

Planning for the distribution of your assets upon your passing can seem a daunting task regardless of the size of your estate. However, planning for how those assets will be distributed, and ensuring your estate plan accounts for your desired distribution, is essential. In this article, we will discuss the

Read More

Kelly Sullivan Joins The Strong Firm P.C. As Senior Counsel

By Bret L. Strong / June 10, 2022

The Strong Firm P.C. is excited to announce the addition of Kelly Sullivan to its team of experienced attorneys. Kelly adds exceptional strength to the firm’s established practice areas based on her wealth of experience in the areas of Litigation, Labor and Employment Law, Business Law and Governmental Law, Zoning

Read More

The Future of Non-Compete Agreements: Executive Order on Promoting Competition in the American Agreement

By Kristina Frankel / April 22, 2022

In July 2021, President Biden signed an Executive Order aiming to limit the use of restrictive covenants in employment relationships. Opening with the premise that “a fair, open, and competitive marketplace has long been a cornerstone of the American economy, while excessive market concentration threatens basic economic liberties, democratic accountability,

Read More

-

Video Vault

Watch videos done by our legal team to gain a better understanding of your legal needs. Our lawyers give video insight into areas such as Real Estate, Business Law, Mergers & Acquisitions and much more.![]()

Contact us