Search Site

1790 Hughes Landing Boulevard, Suite 200 | The Woodlands, Texas 77380

*Commitment Free Inquiry

281-367-1222

A rise or fall in the economy. An adverse legal judgment. Unexpected bills or lack of payments from business partners. A natural disaster. Small businesses face financial blows like these all the time and end up asking the same question: Should my small business consider filing bankruptcy?

Bankruptcy is a legal process for individuals and businesses to use as a means to eliminate or repay debts under the protection of the federal bankruptcy court system.

Before filing for bankruptcy relief, a small business owner should consider these questions:

- Is there another option to filing bankruptcy? Some businesses may have work-out options available with their creditors that will allow them to avoid the bankruptcy process. Believe it or not, it is not always in the best interest of a creditor for their business partner to file bankruptcy.

- Do I need immediate protection of the automatic stay? As soon as the bankruptcy is filed, the debtor is protected by the “automatic stay.” Essentially, this means that creditors who are owed money by the debtor-business are automatically stopped from any payments or attempting to collect payments. Bankruptcy may provide immediate relief to a business who is facing aggressive creditors or collectors.

- Do I want to reorganize or liquidate the business? Liquidation is a means to sell off the assets of the business and pay creditors by priority. Reorganization is a means for paying back creditors by priority and, possibly, restructuring the business. A small business owner must decide what is the end goal.

There are three different types of bankruptcies available to small businesses, depending on the business form and the end goal. For a sole proprietorship, where the owner is responsible for all assets and liabilities of the business, Chapter 7, Chapter 11 or Chapter 13 of the Bankruptcy Code are options. For a corporation or partnership, only Chapter 7 or Chapter 11 are options. The “chapter” that a business files under (i.e. 7, 11 or 13) determines how the case will be administered, as well as the rights of the debtor (entity filing bankruptcy) and creditor(s).

- In Chapter 7, the debtor-business intends to liquidate and the business has no future. A trustee is appointed by the bankruptcy court to take over control of the assets of the debtor-business and distributes the assets among the creditors. After the assets are distributed, the debtor-business receives a bankruptcy “discharge.” A “discharge” is an order from the court that releases the debtor-business from liability for certain specified types of debts, in turn releasing the debtor-business from legal obligation to pay any discharged debts.

- In Chapter 11, the debtor-business intends to reorganize and continue business operations. The debtor-business must create a plan of reorganization for how the debtor-business will pay its debts. The plan must be approved by the bankruptcy court. Upon confirmation of the plan of reorganization, the debtor-business receives a bankruptcy discharge.

- In Chapter 13, a debtor-business intends to reorganize and continue business operations. Chapter 13 (somewhat similar to Chapter 11) allows the debtor-business to file a plan of reorganization which proposes how and when the debts of the debtor-business will be repaid. Upon completion of the plan payments, the debtor-business receives a bankruptcy discharge.

At the end of the day, bankruptcy is a harsh reality that many small businesses face. The fact that it is common does not make it any easier, though. Fortunately, there are trained professionals who can guide you through the process and help you achieve your legal goals.

If your small business is facing financial difficulties, contact a competent bankruptcy attorney to discuss options and a plan of action for financial relief.

Contact a Dedicated Texas Business Lawyer To Schedule a Consultation

Call 281-367-1222 or contact us online to schedule a meeting.

Recent Blog Posts

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

By The Strong Firm P.C. / March 13, 2024

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

As trusted legal advisors, we understand the complexities and challenges that employers face when navigating the landscape of employment law. With the ever-evolving regulatory environment, it's crucial for employers to stay informed and proactive in addressing legal concerns.

One

Read More

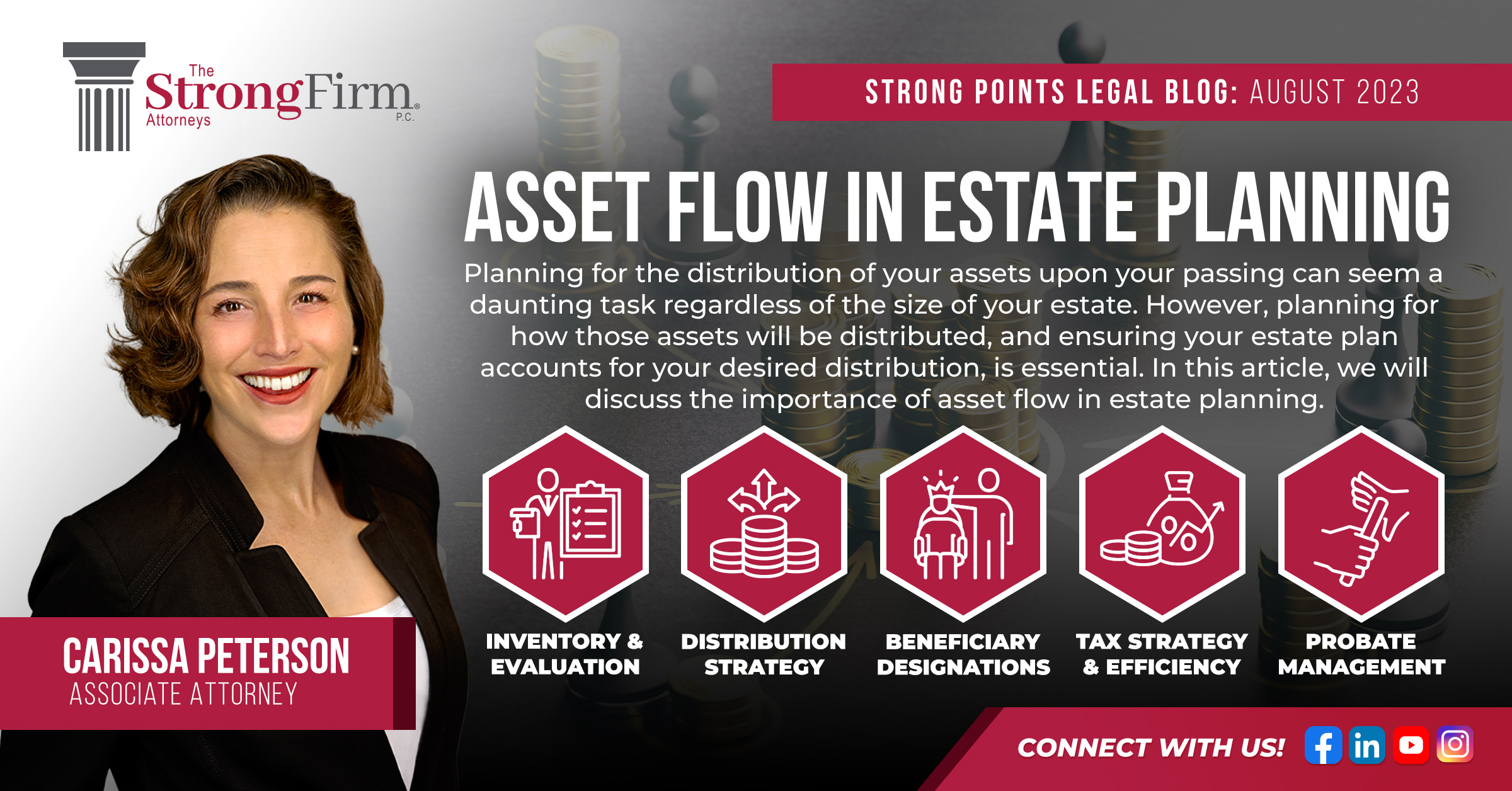

Asset Flow in Estate Planning

By Carissa Peterson / August 21, 2023

Planning for the distribution of your assets upon your passing can seem a daunting task regardless of the size of your estate. However, planning for how those assets will be distributed, and ensuring your estate plan accounts for your desired distribution, is essential. In this article, we will discuss the

Read More

Kelly Sullivan Joins The Strong Firm P.C. As Senior Counsel

By Bret L. Strong / June 10, 2022

The Strong Firm P.C. is excited to announce the addition of Kelly Sullivan to its team of experienced attorneys. Kelly adds exceptional strength to the firm’s established practice areas based on her wealth of experience in the areas of Litigation, Labor and Employment Law, Business Law and Governmental Law, Zoning

Read More

The Future of Non-Compete Agreements: Executive Order on Promoting Competition in the American Agreement

By Kristina Frankel / April 22, 2022

In July 2021, President Biden signed an Executive Order aiming to limit the use of restrictive covenants in employment relationships. Opening with the premise that “a fair, open, and competitive marketplace has long been a cornerstone of the American economy, while excessive market concentration threatens basic economic liberties, democratic accountability,

Read More

-

Video Vault

Watch videos done by our legal team to gain a better understanding of your legal needs. Our lawyers give video insight into areas such as Real Estate, Business Law, Mergers & Acquisitions and much more.![]()

Contact us