Search Site

1790 Hughes Landing Boulevard, Suite 200 | The Woodlands, Texas 77380

*Commitment Free Inquiry

281-367-1222

In Part 3a of our series “The Components of a Business Purchase and Sale from the Buyer’s and Seller’s Perspective” we will discuss the advantages and potential disadvantages of a stock sale from the buyer’s perspective. In a stock sale (or in the event of a limited liability company, a membership interest sale (both called a “stock sale” for the purpose of this article), the seller’s ownership of the company (the “stock”) is what is sold to the seller as opposed to only the assets of the business.

With a stock sale, the buyer takes full ownership of the company, with the company still retaining all of its assets and liabilities. For better or worse, the buyer steps into the shoes of the seller and now owns the entire company and all the good (and bad) that comes along with it. The seller, on the other hand, is now relieved of his or her ownership of the company, with the company retaining all its assets and liabilities. As with any transaction, certain aspects of a stock sale can be negotiated and incorporated in to the sale where certain assets and even liabilities are transfer back to the seller at the closing or immediately before the closing. However, in the most basic of stock sales, the buyer simply replaces the seller as the owner of the company.

As a rule of thumb, stock sales are preferred by sellers while assets sales, as discussed in detail in our previous blogs, are preferred by buyer. Again, the old adage “What’s good for the goose, is good for the gander” is often not true when a stock sale is evaluated from a seller’s or a buyer’s perspective. A more true adage when it comes to the sale of a company is “What’s good for the buyer is bad for the seller”… and vice versa.

In addition to generally being relieved from the ownership of the company with the company retaining all of its debts and obligations, there are often tax advantages for a seller when a transaction is structured as a stock sale verse an asset sale. Assuming the company has operated beyond the required holding period for capital gains purposes, a stock sale should be taxed at the lower capital gains rate. The capital gain or loss for the sale is the difference between the seller’s basis in the stock sold and the sales price. Conversely, the buyer, recognizes no tax until the stock is resold, at which time, the buyer’s basis will be the amount of the purchase price for the stock.

From a closing perspective stock sales tend to be easier transactions as the only item changing ownership is the stock and all company assets, debts, ongoing obligations and contracts stay in possession of the company. In considering a stock sell, however, parties must both be cautious to ensure that there are no contracts to which the company is a party that requires consent from the other contract party if the ownership of the company changes, often called a “Change in Control” provision of a contract.

With any stock sale, buyers and sellers must carefully consider and effectively negotiate the terms and conditions that best serve them. The Strong Firm has assisted countless buyers and sellers alike to ensure that the stock purchase in which they are involved is structured in a manner that best protects them and their investment and we would be happy to assist you as well.

Contact a Dedicated Texas Business Lawyer To Schedule a Consultation

Call 281-367-1222 or contact us online to schedule a meeting.

Recent Blog Posts

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

By The Strong Firm P.C. / March 13, 2024

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

As trusted legal advisors, we understand the complexities and challenges that employers face when navigating the landscape of employment law. With the ever-evolving regulatory environment, it's crucial for employers to stay informed and proactive in addressing legal concerns.

One

Read More

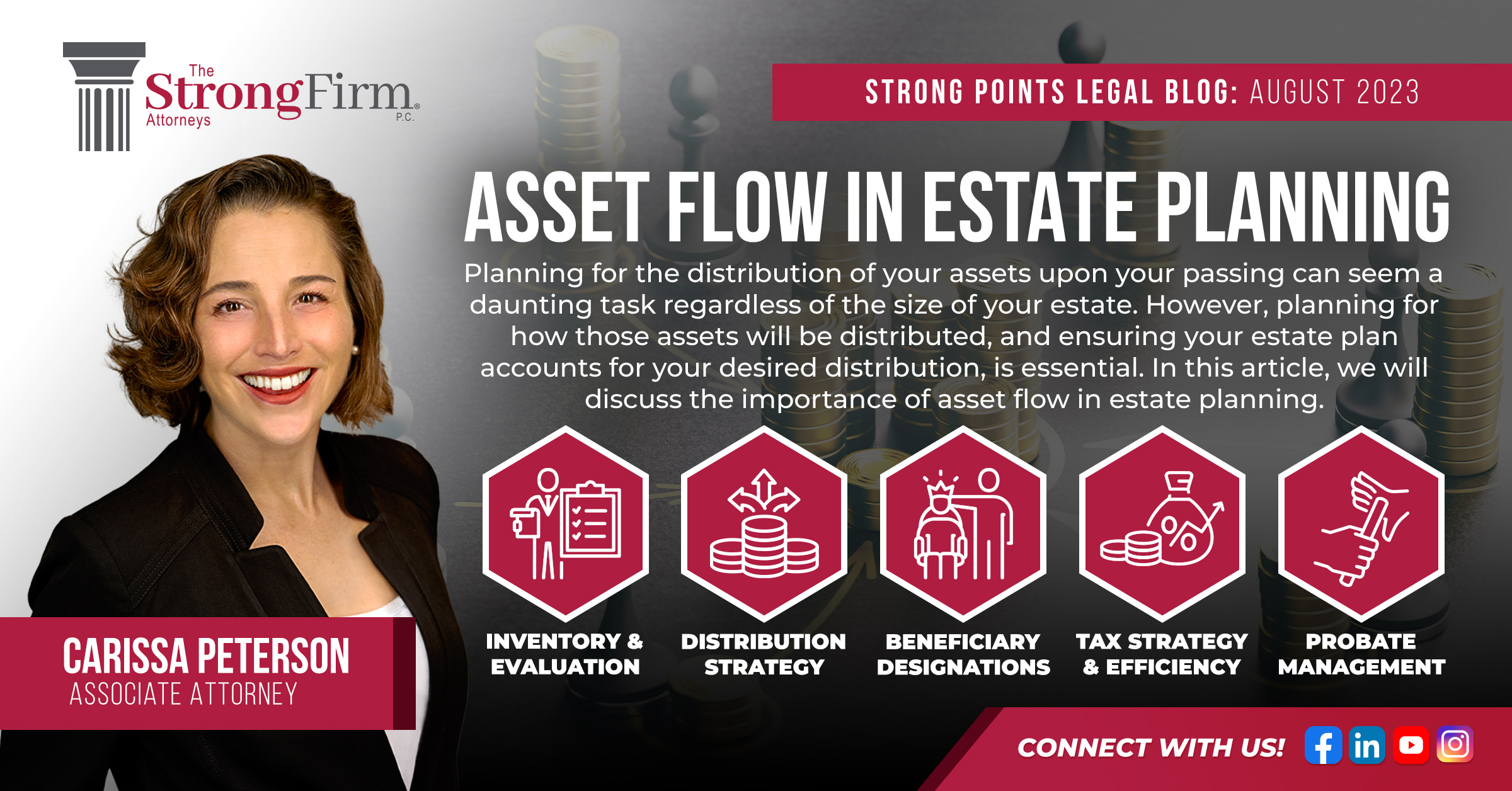

Asset Flow in Estate Planning

By Carissa Peterson / August 21, 2023

Planning for the distribution of your assets upon your passing can seem a daunting task regardless of the size of your estate. However, planning for how those assets will be distributed, and ensuring your estate plan accounts for your desired distribution, is essential. In this article, we will discuss the

Read More

Kelly Sullivan Joins The Strong Firm P.C. As Senior Counsel

By Bret L. Strong / June 10, 2022

The Strong Firm P.C. is excited to announce the addition of Kelly Sullivan to its team of experienced attorneys. Kelly adds exceptional strength to the firm’s established practice areas based on her wealth of experience in the areas of Litigation, Labor and Employment Law, Business Law and Governmental Law, Zoning

Read More

The Future of Non-Compete Agreements: Executive Order on Promoting Competition in the American Agreement

By Kristina Frankel / April 22, 2022

In July 2021, President Biden signed an Executive Order aiming to limit the use of restrictive covenants in employment relationships. Opening with the premise that “a fair, open, and competitive marketplace has long been a cornerstone of the American economy, while excessive market concentration threatens basic economic liberties, democratic accountability,

Read More

-

Video Vault

Watch videos done by our legal team to gain a better understanding of your legal needs. Our lawyers give video insight into areas such as Real Estate, Business Law, Mergers & Acquisitions and much more.![]()

Contact us