Search Site

1790 Hughes Landing Boulevard, Suite 200 | The Woodlands, Texas 77380

*Commitment Free Inquiry

281-367-1222

Part 4c – The Income Approach of Valuing a Business for Sale

In Part 4c of our series “The Components of a Business Purchase and Sale from the Buyer’s and Seller’s Perspective” we will look at the “Income Valuation” approach as the second of three valuation methods for buying a business to be reviewed in this blog series.

As previously discussed, the old adage “What’s good for the goose, is good for the gander” may not ring true when it is applied to the purchase and sale of a business. Oftentimes, “What’s good for the buyer is bad for the seller… and vice versa” is a more accurate statement when it relates to the buying or selling of a business.

One of the fundamental aspects of a business sale is how much is being paid for the business. Valuing the business as a prime example of the “Good for the seller, bad for the buyer or vice versa” adage. It is no surprise that in the sale of a business, the Seller wants to sell the business for as much as possible and the buyer wants to pay as little as possible. Often, the purchase price ultimately agreed to by the parties is a meeting somewhere in the middle. Reaching that valuation, however, often requires a mixture of an evaluation of the business, the assets, and the market and a bit of old fashioned negotiating and horse trading

Of all of the three valuation methods that will be discussed in this blog series (the asset approach, the income approach, and the market approach), the income approach is often a popular approach because at its core, the valuation is based on what is typically the main reason for starting or buying a business, which is generating income. Though the basis for this value is straight forward, the income of the business, how you actually calculate that income, and how you ultimately use that number to determine the value is where this method gets tricky.

Questions such as, “What is considered true income?” “Are there other benefits that the owner is getting that may not be reflected as ‘income’ that should be considered?” and “Can past income levels be reasonably expected in the future particularly if the sale takes place?” To work through these questions in a practical sense, we will return to our example of Sal’s Ice Cream Shop from the previous month’s Blog wherein the asset approach of valuation was discussed. In this example Bob is considering buying the neighborhood ice cream shop from Sal, and Bob as buyer and Sal as seller are attempting to reach an agreement as to the purchase price of Sal’s Ice Cream Shop.” Using the income valuations method again appears pretty straight forward – determine how much income the shop is generating and use that number to determine a valuation of the business. What sounds simple, however, oftentimes is not, particularly when dealing with the purchase or sale of a business.

In our example, in simply looking at the books of Sal’s Ice Cream Shop, one may be surprised to see that the shop only shows a profit “on the books” of $30,000.00 a year. Many people would think that buying a business that is only “making” $30,000.00 a year would not be a good purchase particularly if the asking price for the business is $60,000.00 or even $90,000.00. A close examination of the books, however, would be warranted. While the shop may only be showing $30,000 a year a profit, that is not the only important number to look at. For example, if Sal is drawing a salary of $250,000 a year from the shop as its president and CEO and if Sal’s wife, Sally, is also earning another $250,000 a year from the shop as its CFO, and Sal’s Ferrari, and Sally’s Rolls Royce are being paid through the company as business expenses as “company cars”, then all of sudden, the true “income” potential for this business is viewed in a completely different light. In that instance, Sal would argue that while the “profits” of the company may only be $30,000.00 annually, the company is truly generating much more than that especially when you consider the $500,000 in annual salaries being paid to Sal and Sally and the expensive vehicles that are being paid for as company cars. Accordingly, Sal would likely argue that these amounts should be considered when determining the “income” of the company, and the asking price of the business will likely be 30 times the $30,000 year end profits being reported or even more. For this reason when determining the best number to use for the income valuation number, a figure called EBITDA is often used. The used of EBITDA, which means “Earnings Before Interest, Taxes, Depreciation and Amortization” however, is not without controversy because this number may not provide the most accurate portrayal of the “true” numbers of the business. Regardless of the methods of valuation being considered, the potential buyer and seller should each employ their own accountant to review the books of the company to assist in reaching a valuation.

Another item regarding income that a potential buyer should consider is, “Can the revenue being generated be reasonably expected should the sale take place?” While no one has a crystal ball to tell the future, a potential buyer should very seriously and objectively consider the likelihood of the business’ ability to continue generating the revenue it has generated in the past. Was Sal’s Ice Cream Shop so successful because the customers knew that every time they came in the shop they would be personally greeted by Sal and Sally’s smiling faces? Were customers coming to the shop more so for Sal’s grand personality and funny stories than for the ice cream? Did Sal and Sally’s enormous extended family and friends account for a majority of the sales at the shop? If the answer to any of these questions is yes, then the Buyer should carefully consider if the customers will continue to visit the shop once Sal and Sally have sold the business. If so, looking at the past revenue of the shop may not be an effective method of determining the value of the business, because those revenue numbers may not be obtainable if Sal were to sell the shop.

As previously discussed, due to the many variables involved in something as “simple” as reaching a purchase price for a business it is important that anyone considering buying or selling a business use experienced and qualified legal counsel. The Strong Firm has assisted hundreds of buyers and sellers in all steps involved in buying or selling a business and we would be glad to do the same for you.

Contact a Dedicated Texas Business Lawyer To Schedule a Consultation

Call 281-367-1222 or contact us online to schedule a meeting.

Recent Blog Posts

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

By The Strong Firm P.C. / March 13, 2024

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

As trusted legal advisors, we understand the complexities and challenges that employers face when navigating the landscape of employment law. With the ever-evolving regulatory environment, it's crucial for employers to stay informed and proactive in addressing legal concerns.

One

Read More

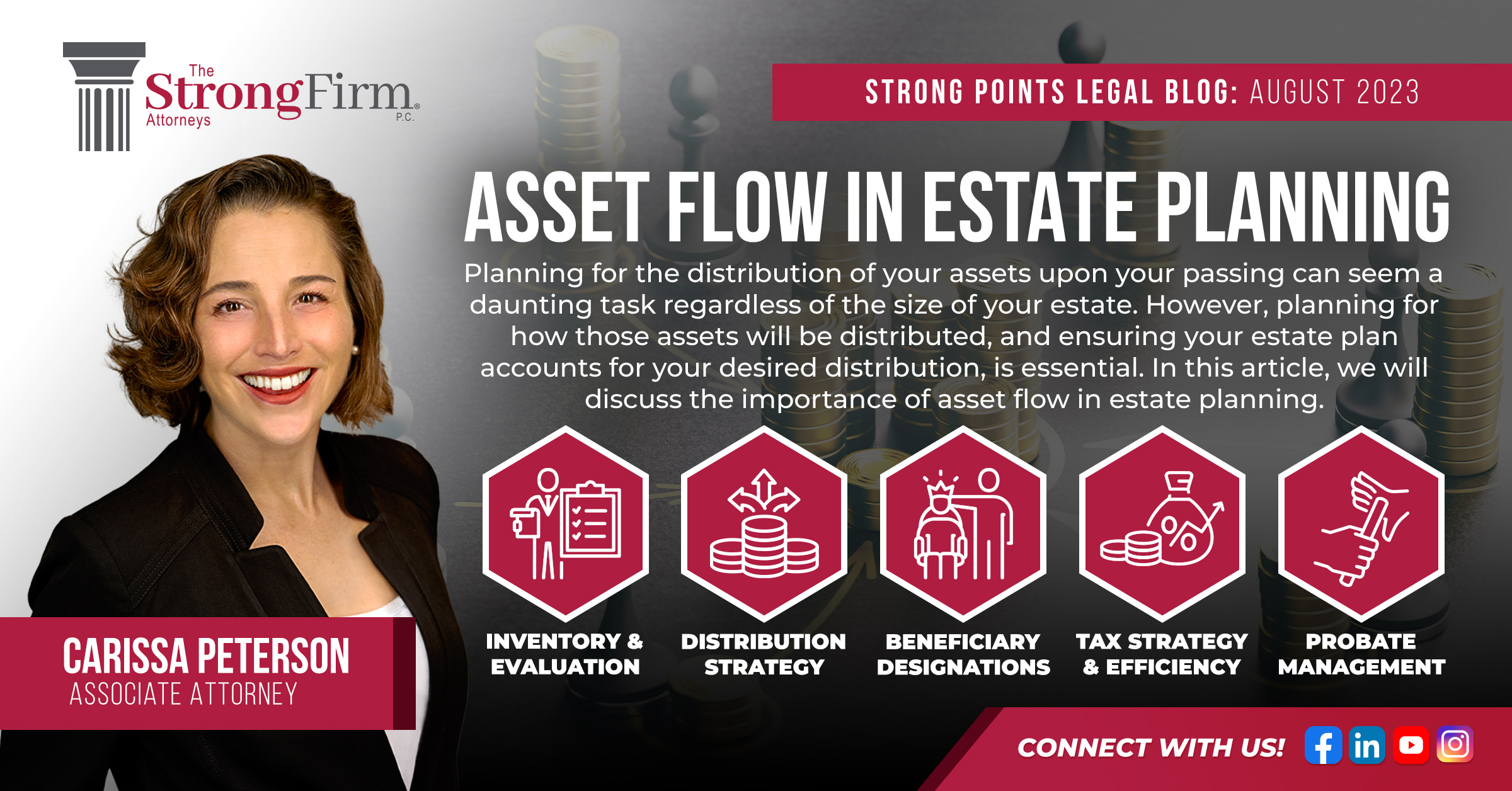

Asset Flow in Estate Planning

By Carissa Peterson / August 21, 2023

Planning for the distribution of your assets upon your passing can seem a daunting task regardless of the size of your estate. However, planning for how those assets will be distributed, and ensuring your estate plan accounts for your desired distribution, is essential. In this article, we will discuss the

Read More

Kelly Sullivan Joins The Strong Firm P.C. As Senior Counsel

By Bret L. Strong / June 10, 2022

The Strong Firm P.C. is excited to announce the addition of Kelly Sullivan to its team of experienced attorneys. Kelly adds exceptional strength to the firm’s established practice areas based on her wealth of experience in the areas of Litigation, Labor and Employment Law, Business Law and Governmental Law, Zoning

Read More

The Future of Non-Compete Agreements: Executive Order on Promoting Competition in the American Agreement

By Kristina Frankel / April 22, 2022

In July 2021, President Biden signed an Executive Order aiming to limit the use of restrictive covenants in employment relationships. Opening with the premise that “a fair, open, and competitive marketplace has long been a cornerstone of the American economy, while excessive market concentration threatens basic economic liberties, democratic accountability,

Read More

-

Video Vault

Watch videos done by our legal team to gain a better understanding of your legal needs. Our lawyers give video insight into areas such as Real Estate, Business Law, Mergers & Acquisitions and much more.![]()

Contact us