Search Site

1790 Hughes Landing Boulevard, Suite 200 | The Woodlands, Texas 77380

*Commitment Free Inquiry

281-367-1222

Part 4b – The Asset Valuation Approach of Valuing a Business for Sale

In Part 4b of our series “The Components of a Business Purchase and Sale from the Buyer’s and Seller’s Perspective” we will look at the Asset Valuation approach as the first of three valuation methods for buying a business to be reviewed in this blog series.

The common theme we have discussed throughout the series is that old adage “What’s good for the goose, is good for the gander” is often not true when discussing the purchase and sale of a business, but rather when buying and selling a business a more accurate adage is “What’s good for the buyer is often bad for the seller… and vice versa”.

Once the question, “What is being sold (stock sale or asset sale)?” is answered, as discussed in our previous blogs, the next question that buyer and seller will need to answer is “How much will you pay?” As with most business matters there is not a clear cut “right” answer and the valuation method and amount can vary greatly depending on a) stock sale vs. asset sale, b) who is determining the valuation (buyer or seller) and c) the valuation method being utilized.

The Asset Valuation approach, on its face, appears to be a straight forward “balance sheet” approach of calculating value by taking any assets being purchased, subtracting out any liabilities being assumed and the difference give you the value of the business. As with most other aspects of a business sale, the challenge lies in the details. If the sale is an asset sale and the only assets being purchased are physical tangible assets with set or easily determinable values, (i.e. vehicles, commonly used machinery and tools, commercial real estate, and even accounts receivables with no discounting) then determining the value using an Asset Valuation approach is straight forward and is often mutually fair to buyer and seller. The problem, of course, is that a business purchase solely consisting of an asset purchase where all of the assets are physical tangible assets with set or easily determinable values is rare. Often times, business sales include a portion of these types of assets, but also can include intangible assets, such as a trademark, social media presence and following, goodwill, interest in a leasehold, and even common law rights to the business’ tradename and logos. A business possessing these intangible assets is much more difficult to value using a straight Asset Valuation approach and it is not uncommon for the buyer and seller to have wildly different ideas on what these intangibles are worth.

Ultimately the buyer and seller will need to come to some agreement as to what is actually being purchased, not in the sense of a list of assets being purchased, but the true “spirit” of the transaction. As an example, Bob wants to buy Sal’s Ice Cream Shop, a shop that has been in the community for the last 30 years. Sal agrees to sell to Bob. What is it that Bob truly desires to purchase? Is it the turnkey business that Sal has established? Does Bob plan to keep everything the same, including the name and to continue operating the business as if Sal never left? In that case, it is likely that Sal would seek and Bob would be willing to pay a higher value for the intangible assets that Sal’s Ice Cream Shop possesses, such as the name recognition of “Sal’s Ice Cream Shop”, a loyal customer base, and a solid history/reputation in the community. If Bob’s plan for purchasing Sal’s business is to take the equipment and move it over to Bob’s existing ice cream store across town, or to stay at Sal’s current location, keep the equipment in place, but completely change the store design, the store name, and even the products sold, then Bob would likely want to value this purchase using a straight Asset Valuation approach, wherein Bob is giving value for the physical tangible assets (equipment) and little to no value for the intangibles such as trade name, reputation, goodwill. These intangibles would have little if any value to Bob, as he plans on ending Sal’s Ice Cream Shop and all of the goodwill, customer loyalty, and history in the community that comes with it, and opening up a brand new store.

At the end of the day, determining if the Asset Value approach is the best method to value the business being sold, will ultimately require a meeting of the minds of the buyer and seller based on their respective positions. Fortunately if a straight Asset Value approach is not the best method of valuing a business sale, there are other methods of determining value that may be more applicable depending on the transaction at hand, including the Income approach and Market approach or even a hybrid of two or all three of these methods which will be discussed in future blogs.

Because of the variables at a play with something as seemingly simple as determining a sales price, buying or selling a business, even something straight forward as an ice cream shop can be more complicated than originally suspected. For this reason, it is critical that anyone considering buyer or selling a business obtains experienced and qualified legal counsel. The Strong Firm has assisted hundreds of buyers and sellers alike not only in figuring out the best valuation method, but we have also assisted those same buyers and sellers in all of the other steps involved in buying or selling a business and we would be glad to do the same for you.

Contact a Dedicated Texas Business Lawyer To Schedule a Consultation

Call 281-367-1222 or contact us online to schedule a meeting.

Recent Blog Posts

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

By The Strong Firm P.C. / March 13, 2024

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

As trusted legal advisors, we understand the complexities and challenges that employers face when navigating the landscape of employment law. With the ever-evolving regulatory environment, it's crucial for employers to stay informed and proactive in addressing legal concerns.

One

Read More

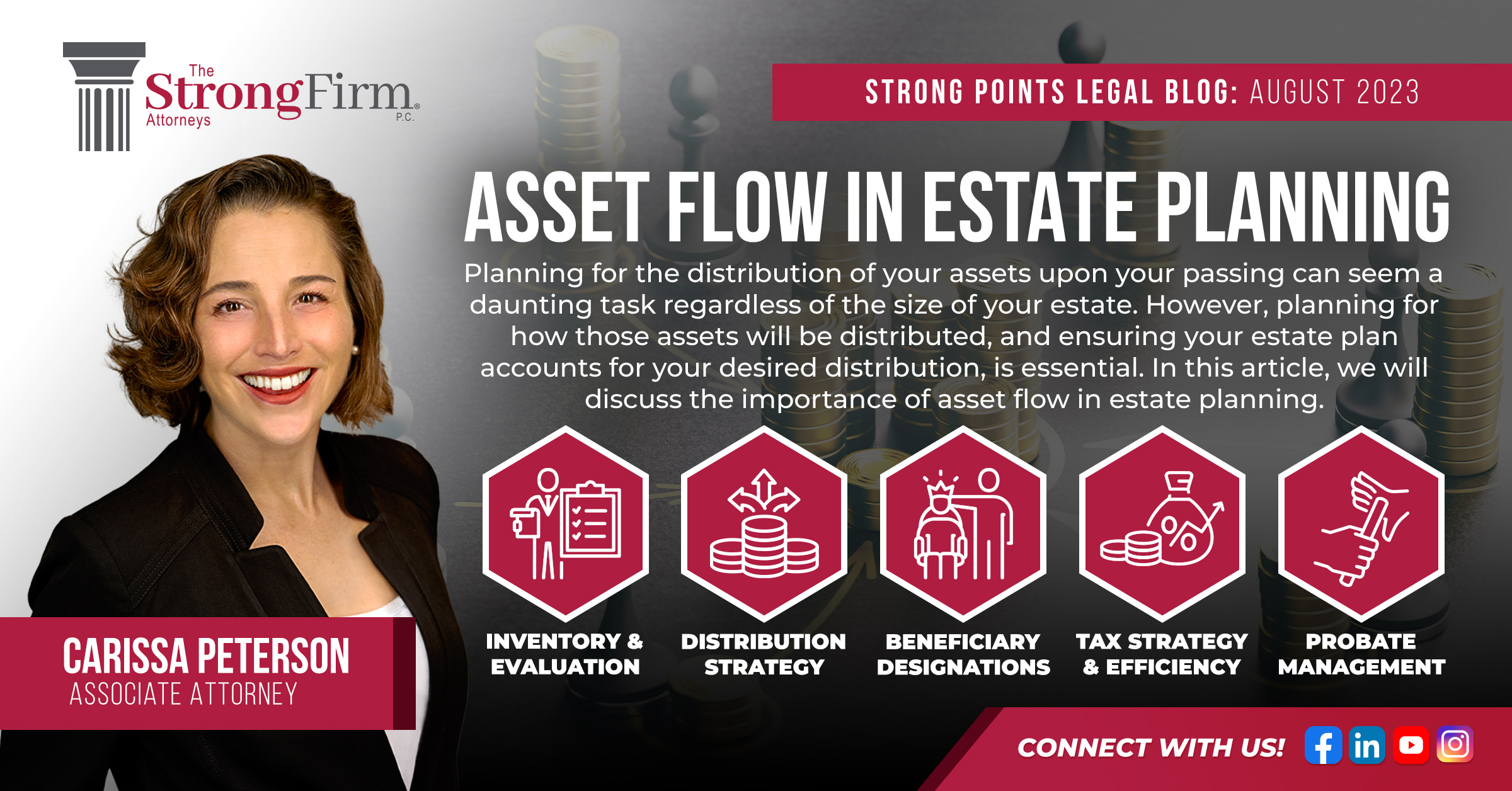

Asset Flow in Estate Planning

By Carissa Peterson / August 21, 2023

Planning for the distribution of your assets upon your passing can seem a daunting task regardless of the size of your estate. However, planning for how those assets will be distributed, and ensuring your estate plan accounts for your desired distribution, is essential. In this article, we will discuss the

Read More

Kelly Sullivan Joins The Strong Firm P.C. As Senior Counsel

By Bret L. Strong / June 10, 2022

The Strong Firm P.C. is excited to announce the addition of Kelly Sullivan to its team of experienced attorneys. Kelly adds exceptional strength to the firm’s established practice areas based on her wealth of experience in the areas of Litigation, Labor and Employment Law, Business Law and Governmental Law, Zoning

Read More

The Future of Non-Compete Agreements: Executive Order on Promoting Competition in the American Agreement

By Kristina Frankel / April 22, 2022

In July 2021, President Biden signed an Executive Order aiming to limit the use of restrictive covenants in employment relationships. Opening with the premise that “a fair, open, and competitive marketplace has long been a cornerstone of the American economy, while excessive market concentration threatens basic economic liberties, democratic accountability,

Read More

-

Video Vault

Watch videos done by our legal team to gain a better understanding of your legal needs. Our lawyers give video insight into areas such as Real Estate, Business Law, Mergers & Acquisitions and much more.![]()

Contact us