Search Site

1790 Hughes Landing Boulevard, Suite 200 | The Woodlands, Texas 77380

*Commitment Free Inquiry

281-367-1222

In Part 2b of our series “The Pros and Cons of Components of a Business Purchase and Sale

from the Buyer’s and Seller’s perspective” we will look at the potential disadvantages a seller could face if the sale of his or her business is structured as an asset purchase as opposed to a stock (in the case of a corporation) or membership interest (in the case of an LLC) purchase. Specifically, this article 2b will discuss a seller being required to retain certain assets and liabilities from an asset sale.

As previously discussed in this series “What’s Good for the Goose…” the purchase and sale of business can take place as either by the stock or membership interest (in the case of an LLC) purchase or as an asset purchase. Generally, buyers tend to prefer that the transaction be structured as an asset sale which allows the buyer to pick and choose the business assets the buyer wants while keeping the less desired or “troubled” assets with the seller and the buyer choosing not to assume any, or very little, of the business’ liabilities. As was stated in the prior articles in this series “Oftentimes, what is good for the buyer is bad for the seller… and vice versa”

SELLER’S DISADVANTAGES FROM AN ASSET SALE.

Buyer’s Selection of Desirable Assets while Leaving Seller with “Troubled” Assets and Most or All of the Business’ liabilities. By structuring the purchase of a business as an asset sale, the buyer will be able to select the specific assets they prefer and exclude assets that could be problematic or they simply do not want. While this is clearly advantageous for the buyer, it is a distinct disadvantage to the seller of the business. Typically, when a business owner is looking to sell their business, they are doing so, at least in part, to get out of that particular business. In a business sale that it structured as an asset sale, the buyer is able to pick and choose the business’ asset they desire to acquire from the business leaving the seller with the undesired and potentially troublesome assets. Problemed assets can include anything from damaged, aging, or outdated equipment, to difficult or underperforming client accounts, to intellectual property that is the subject matter of a lawsuit or a claim. While it is understandable why a buyer would not want to inherit these headache assets, sellers looking to sell their business or exit the trade all together may find themselves with some very unattractive and difficult assets on their hands even after the sale of the business. If the transaction were structured as a stock or membership interest sale, the buyer automatically assumes title to all of the assets as well as the liabilities of the business by buying all of the stock or membership of the company, resulting in a clear upside for the seller who is then free of all of the assets (including the problemed assets)

Exclusion of Liabilities. Just like with the section of assets discussed above, a transaction structured as an asset purchase also allows a buyer to select which liabilities or obligations, if any, the buyer will take on. Oftentimes the buyer will not assume any liabilities or obligations of the business, leaving the seller to figure out how these remaining liabilities will be settled and closed. In a stock sale, however, any business debt, obligation, or liability becomes the responsibility of the buyer unless expressly excluded in the sale.

When considering any purchase or sale of a business it is critical that each side carefully consider and effectively negotiate the structure which best serves them. Assistance from a law firm familiar with the intricacies of a business sale and purchase, whether structured as an asset sale or a stock sale, is critical to ensure that you are best protected in that transaction.

Contact a Dedicated Texas Business Lawyer To Schedule a Consultation

Call 281-367-1222 or contact us online to schedule a meeting.

Recent Blog Posts

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

By The Strong Firm P.C. / March 13, 2024

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

As trusted legal advisors, we understand the complexities and challenges that employers face when navigating the landscape of employment law. With the ever-evolving regulatory environment, it's crucial for employers to stay informed and proactive in addressing legal concerns.

One

Read More

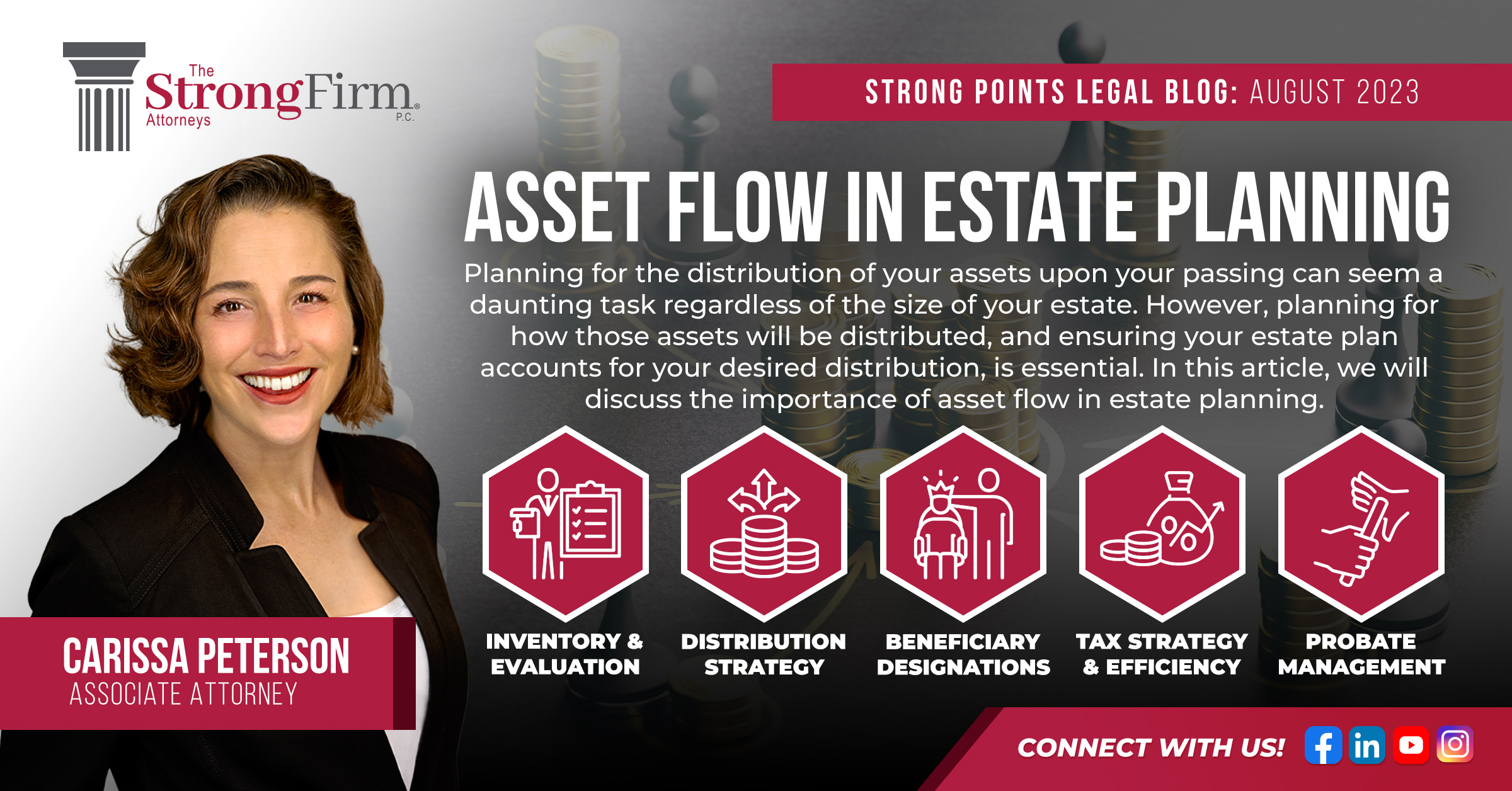

Asset Flow in Estate Planning

By Carissa Peterson / August 21, 2023

Planning for the distribution of your assets upon your passing can seem a daunting task regardless of the size of your estate. However, planning for how those assets will be distributed, and ensuring your estate plan accounts for your desired distribution, is essential. In this article, we will discuss the

Read More

Kelly Sullivan Joins The Strong Firm P.C. As Senior Counsel

By Bret L. Strong / June 10, 2022

The Strong Firm P.C. is excited to announce the addition of Kelly Sullivan to its team of experienced attorneys. Kelly adds exceptional strength to the firm’s established practice areas based on her wealth of experience in the areas of Litigation, Labor and Employment Law, Business Law and Governmental Law, Zoning

Read More

The Future of Non-Compete Agreements: Executive Order on Promoting Competition in the American Agreement

By Kristina Frankel / April 22, 2022

In July 2021, President Biden signed an Executive Order aiming to limit the use of restrictive covenants in employment relationships. Opening with the premise that “a fair, open, and competitive marketplace has long been a cornerstone of the American economy, while excessive market concentration threatens basic economic liberties, democratic accountability,

Read More

-

Video Vault

Watch videos done by our legal team to gain a better understanding of your legal needs. Our lawyers give video insight into areas such as Real Estate, Business Law, Mergers & Acquisitions and much more.![]()

Contact us