Search Site

1790 Hughes Landing Boulevard, Suite 200 | The Woodlands, Texas 77380

*Commitment Free Inquiry

281-367-1222

In recent years, it has become increasingly important to consider the income tax implications of gift giving and not just the estate tax implications. For the majority of people, estate taxes are a non-issue due to the increase in the exclusion amount for US citizens. However, income tax continues to impact everyone. Therefore, an estate plan that is designed to optimize the income tax benefits to your heirs may have significantly more value than an estate plan focused solely on estate taxes.

The White House has identified the step-up in basis on capital assets as the “single largest capital gains tax loophole.”[1] What is this loop hole you ask? It is usually easiest to show with an example. Imagine you have purchased stock in Google for $10,000 and over the years it has appreciated to $100,000. If you sell that stock during your life the IRS will calculate the income taxes owed by subtracting your $10,000 basis from stock’s current fair market value of $100,000 which equals $90,000 [i.e. $100,000 – $10,000 = $90,000] of taxable income that can be taxed at a rate as high as 23.8% (or $21,420 in taxes owed).

Under this example, the capital gains taxes are more than twice as much as you originally paid for the Google stock. Likewise, if you give that stock to your descendant while you are alive, then the recipient of that gift gets your original $10,000 basis and will have to perform the same capital gains calculation when they go to sell the asset.

By contrast, if a person dies owning that same stock there is a step-up in basis to the fair market value of the asset on the date of the owner’s death. So if the stock is then worth $100,000 the new basis on the asset is $100,000 and the taxable income is $0.00 [i.e. $100,000 – $100,000 = $0]. With proper planning, this step-up in basis can occur again when the surviving spouse in a marriage passes providing your descendants with a second step-up in basis.

However, many older estate plans were designed to minimize estate taxes at the expense of maximizing the step-up in basis. Accordingly, if you are holding on to older estate planning documents it is time to get in front of your estate planning attorney and make sure that your tax planning is still current in light of the changes in the tax law.

Royce Lanning

Phone: 281-367-1222

Fax: 281-210-1361

Contact a Dedicated Texas Business Lawyer To Schedule a Consultation

Call 281-367-1222 or contact us online to schedule a meeting.

Recent Blog Posts

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

By The Strong Firm P.C. / March 13, 2024

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

As trusted legal advisors, we understand the complexities and challenges that employers face when navigating the landscape of employment law. With the ever-evolving regulatory environment, it's crucial for employers to stay informed and proactive in addressing legal concerns.

One

Read More

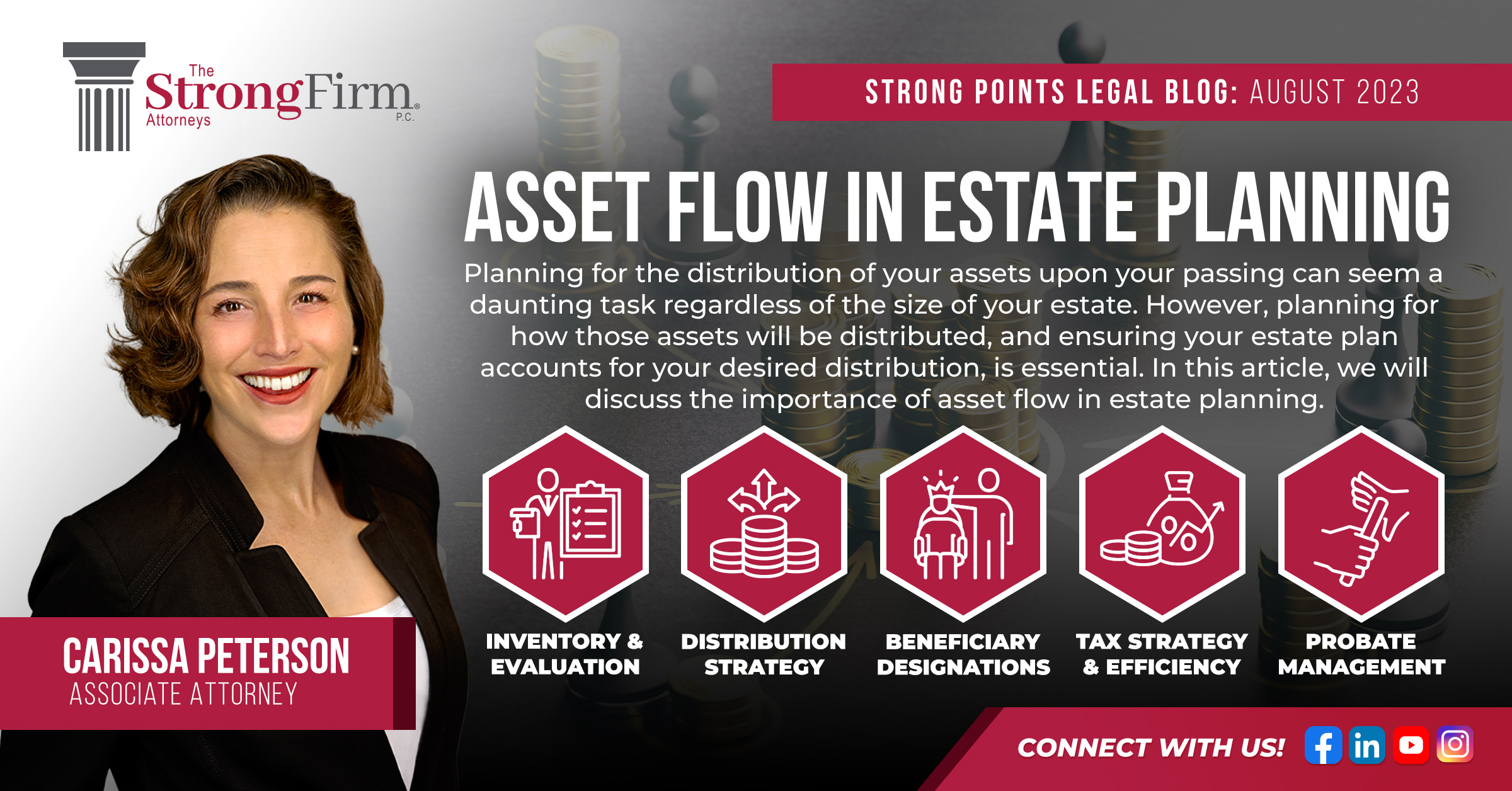

Asset Flow in Estate Planning

By Carissa Peterson / August 21, 2023

Planning for the distribution of your assets upon your passing can seem a daunting task regardless of the size of your estate. However, planning for how those assets will be distributed, and ensuring your estate plan accounts for your desired distribution, is essential. In this article, we will discuss the

Read More

Kelly Sullivan Joins The Strong Firm P.C. As Senior Counsel

By Bret L. Strong / June 10, 2022

The Strong Firm P.C. is excited to announce the addition of Kelly Sullivan to its team of experienced attorneys. Kelly adds exceptional strength to the firm’s established practice areas based on her wealth of experience in the areas of Litigation, Labor and Employment Law, Business Law and Governmental Law, Zoning

Read More

The Future of Non-Compete Agreements: Executive Order on Promoting Competition in the American Agreement

By Kristina Frankel / April 22, 2022

In July 2021, President Biden signed an Executive Order aiming to limit the use of restrictive covenants in employment relationships. Opening with the premise that “a fair, open, and competitive marketplace has long been a cornerstone of the American economy, while excessive market concentration threatens basic economic liberties, democratic accountability,

Read More

-

Video Vault

Watch videos done by our legal team to gain a better understanding of your legal needs. Our lawyers give video insight into areas such as Real Estate, Business Law, Mergers & Acquisitions and much more.![]()

Contact us