Search Site

1790 Hughes Landing Boulevard, Suite 200 | The Woodlands, Texas 77380

*Commitment Free Inquiry

281-367-1222

Thinking about starting a new or buying an existing business? While that decision is undoubtedly a hard one, the next decision can be equally, if not even more, difficult.

How do I pay for it? How to fund the purchase of a business is a question that we have helped clients through countless times at The Strong Firm P.C.

Small Business Association (SBA) loans are a viable option for some new small business owners. Unlike with a grant, a SBA loan does have to be repaid.

One common misconception about SBA loans is that they are very easy to obtain since they are “guaranteed” by the federal government. While it is true that the SBA loan program may provide an opportunity for an individual or small business to obtain funding that it would not normally be able to procure through normal channels, the process is not “easy” by any means.

To secure an SBA loan the lender will review two factors: the strength of the business and more importantly the credit strength of the borrower/owner. To this end, borrowers will find it much easier to obtain funding for the acquisition of an existing business with a proven track record than attempting to fund an unproven “startup company” with no financial history.

In analyzing the strength of the business the lender will typically require 1) a formal business plan describing the nature of the business, annual sales, number of employees, length of time in business and ownership of the business and 2) business financial statements including complete financial statements for the past three years and current interim financial statements.

In evaluating the strength of the borrower, banks will require and will examine the personal financial statements of the owners, partners, officers and stockholders owning 20% or more of the business.

Contrary to the beliefs of many new business owners, it is almost impossible to establish “business credit” for your new business that is not directly and heavily tied to your personal finances. A lender will also typically further require a personal guaranty from any and all owners of the company.

Eric R. Thiergood, Sr.

Phone: 281-367-1222

Fax: 281-210-1361

Email: [email protected]

Contact a Dedicated Texas Business Lawyer To Schedule a Consultation

Call 281-367-1222 or contact us online to schedule a meeting.

Recent Blog Posts

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

By The Strong Firm P.C. / March 13, 2024

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

As trusted legal advisors, we understand the complexities and challenges that employers face when navigating the landscape of employment law. With the ever-evolving regulatory environment, it's crucial for employers to stay informed and proactive in addressing legal concerns.

One

Read More

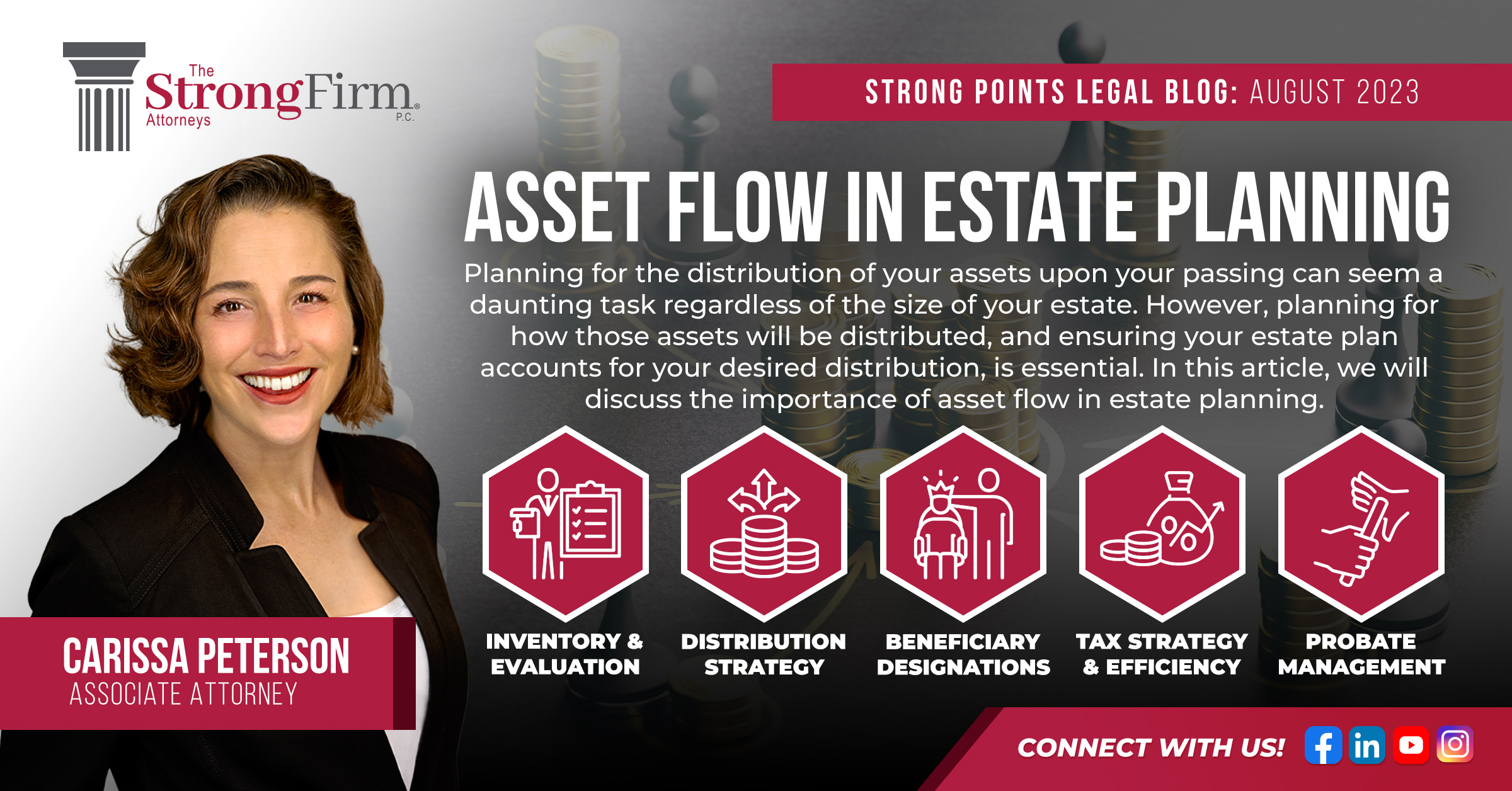

Asset Flow in Estate Planning

By Carissa Peterson / August 21, 2023

Planning for the distribution of your assets upon your passing can seem a daunting task regardless of the size of your estate. However, planning for how those assets will be distributed, and ensuring your estate plan accounts for your desired distribution, is essential. In this article, we will discuss the

Read More

Kelly Sullivan Joins The Strong Firm P.C. As Senior Counsel

By Bret L. Strong / June 10, 2022

The Strong Firm P.C. is excited to announce the addition of Kelly Sullivan to its team of experienced attorneys. Kelly adds exceptional strength to the firm’s established practice areas based on her wealth of experience in the areas of Litigation, Labor and Employment Law, Business Law and Governmental Law, Zoning

Read More

The Future of Non-Compete Agreements: Executive Order on Promoting Competition in the American Agreement

By Kristina Frankel / April 22, 2022

In July 2021, President Biden signed an Executive Order aiming to limit the use of restrictive covenants in employment relationships. Opening with the premise that “a fair, open, and competitive marketplace has long been a cornerstone of the American economy, while excessive market concentration threatens basic economic liberties, democratic accountability,

Read More

-

Video Vault

Watch videos done by our legal team to gain a better understanding of your legal needs. Our lawyers give video insight into areas such as Real Estate, Business Law, Mergers & Acquisitions and much more.![]()

Contact us