Search Site

1790 Hughes Landing Boulevard, Suite 200 | The Woodlands, Texas 77380

*Commitment Free Inquiry

281-367-1222

Is your “independent contractor” actually an employee? While it seems like a relatively simple question, the ramifications are substantial to a business owner. Misclassifying and paying a worker as a 1099 independent contractor, when in reality he or she should be treated as a W2 employee, can result in a variety of consequences for the employer. Misclassifying a worker often means the employer has also failed to pay the proper amount of employment taxes on that person. By withholding the incorrect employment taxes, the burden of those additional taxes is improperly shifted to the employee.

The reasons employees are misclassified as independent contractors can range from a simple mistake to a much more nefarious reason for financial gain. At times, it is the contractor/employee who requests or prefers to be paid as a 1099 contractor, rather than a W2 employee, because his or her paycheck will typically be higher since no taxes are withheld. However, though this will result in a higher pay check initially, in the end the worker will be hit with higher tax liability when they file their annual income taxes and are responsible for paying self-employment taxes. Employers must always remember that regardless of what a worker wants or prefers, it is the employer’s responsibility to properly classify the contractor/employee status of its workers.

Some employers prefer to treat and pay all workers as 1099 contractors because they simply find it easier on the HR and administrative side. Other employers have a purely financial motivation for the misclassification as independent contractors are not entitled to overtime pay, unemployment benefits and are not typically covered by worker’s compensation insurance. For these reasons, some employers who are willing to push the line of illegal and unethical business practices will intentionally and knowingly misclassify workers as independent contractors rather than employees for financial gain. Regardless of the motivation and intent, the misclassification of a worker will create a number of headaches for employers.

Businesses are facing increased scrutiny from at least three separate state and federal agencies: the Texas Workforce Commission, the Texas Office of the Comptroller of Public Accounts, and the United States Internal Revenue Service (“IRS”). Misclassification of workers most often results in the underreporting and underpaying of various state and federal employment and income taxes, which understandably supplies the motivation for these agencies to aggressively investigate and uncover businesses who have misclassified their workers. Failure or refusal by an employer to properly classify its workers can subject it to a number of state and federal civil penalties. Moreover, an employee who has been mischaracterized may be entitled to between 2 and 3 years’ worth of unpaid overtime once the misclassification is discovered.

Eric R. Thiergood, Sr.

Phone: 281-367-122

Fax: 281-210-1361

Contact a Dedicated Texas Business Lawyer To Schedule a Consultation

Call 281-367-1222 or contact us online to schedule a meeting.

Recent Blog Posts

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

By The Strong Firm P.C. / March 13, 2024

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

As trusted legal advisors, we understand the complexities and challenges that employers face when navigating the landscape of employment law. With the ever-evolving regulatory environment, it's crucial for employers to stay informed and proactive in addressing legal concerns.

One

Read More

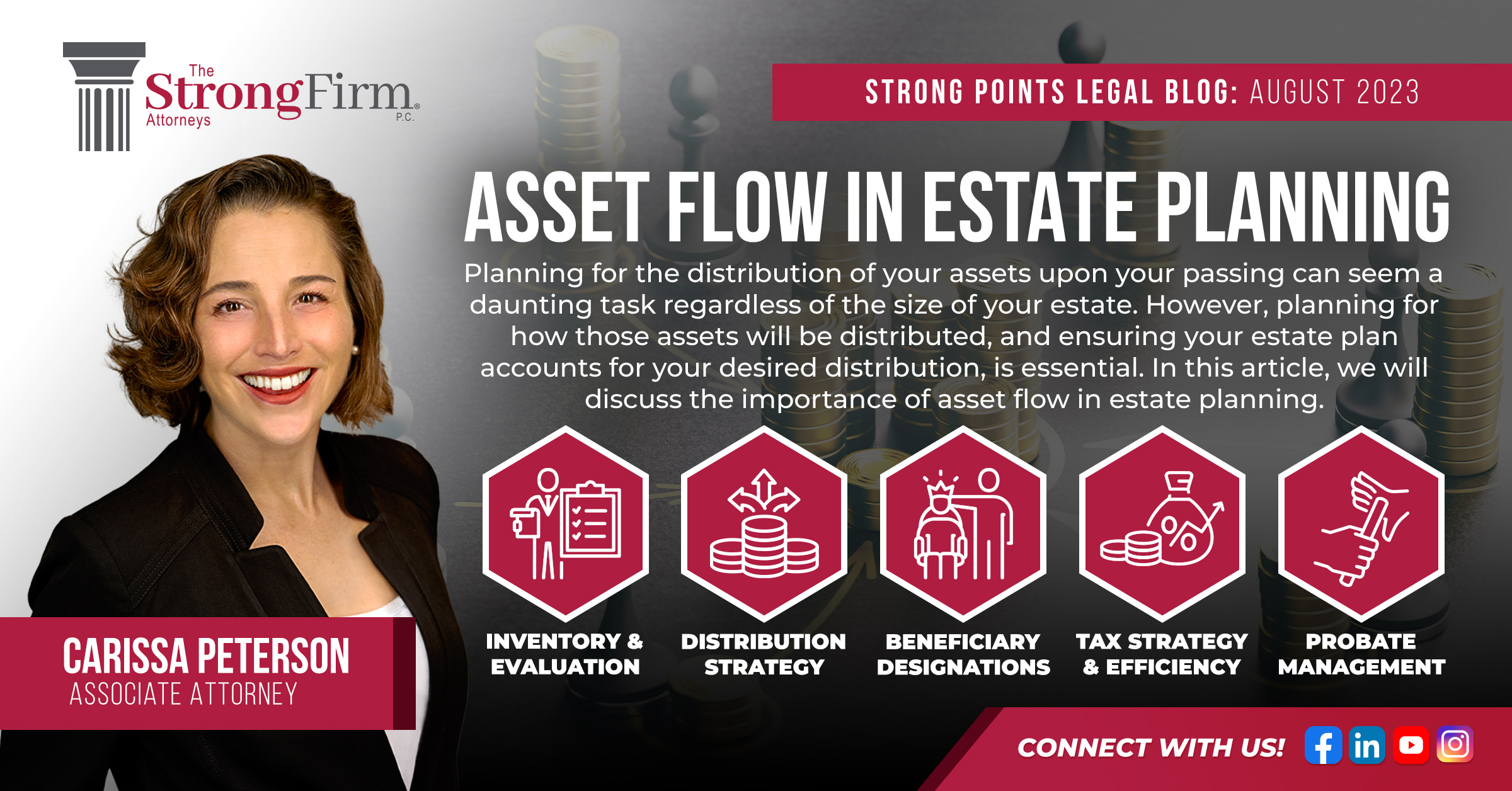

Asset Flow in Estate Planning

By Carissa Peterson / August 21, 2023

Planning for the distribution of your assets upon your passing can seem a daunting task regardless of the size of your estate. However, planning for how those assets will be distributed, and ensuring your estate plan accounts for your desired distribution, is essential. In this article, we will discuss the

Read More

Kelly Sullivan Joins The Strong Firm P.C. As Senior Counsel

By Bret L. Strong / June 10, 2022

The Strong Firm P.C. is excited to announce the addition of Kelly Sullivan to its team of experienced attorneys. Kelly adds exceptional strength to the firm’s established practice areas based on her wealth of experience in the areas of Litigation, Labor and Employment Law, Business Law and Governmental Law, Zoning

Read More

The Future of Non-Compete Agreements: Executive Order on Promoting Competition in the American Agreement

By Kristina Frankel / April 22, 2022

In July 2021, President Biden signed an Executive Order aiming to limit the use of restrictive covenants in employment relationships. Opening with the premise that “a fair, open, and competitive marketplace has long been a cornerstone of the American economy, while excessive market concentration threatens basic economic liberties, democratic accountability,

Read More

-

Video Vault

Watch videos done by our legal team to gain a better understanding of your legal needs. Our lawyers give video insight into areas such as Real Estate, Business Law, Mergers & Acquisitions and much more.![]()

Contact us