Search Site

1790 Hughes Landing Boulevard, Suite 200 | The Woodlands, Texas 77380

*Commitment Free Inquiry

281-367-1222

There are a number of motivations to give a gift to loved ones during life; however, it is important to remember that certain assets are taxed more favorably if they are given after the owner’s death. As discussed in my recent blog post, The “Basis” for Good Planning: Using “Stepped-Up” Basis to Reduce Taxes, assets that are subject to long-term capital gains are granted a significant income tax advantage, a “step-up” in basis, if they are held until the owner’s death.[1]

First generation business owners may be presented with this issue when they want to give their children a current stake in the company that they have built. While nothing is more natural then wanting to watch our children succeed during our lifetime, with planning we may be able to achieve some underlying practical goals while still utilizing the tax advantages presented by holding a significant portion of the asset’s value until death. For instance, by utilizing a well-structured shareholder agreement, business owners can grant their child a minimal interest in the business and a position in the company as a means to (1) establishing the child’s role in the business, (2) train the child to manage the business, (3) provide a current income stream and job stability, and/or (4) provide the child an immediate incentive to focus on the business’ success. By granting the child a minimal stake in the company, the business owner has have both created a structure to transfer the company at the time of your passing and maintained the bulk of the asset’s value in your hands in order to capitalize on the capital gains tax advantages associated with a step-up in basis.

Although this type of planning must be carefully weighed against the estate tax advantages presented by certain types of lifetime transfers, in the right circumstances, the advantages of the “step-up” in basis may outweigh the estate tax benefits of certain lifetime transfers. Accordingly, before making a substantial gift of your assets it is important to first identify any extraneous or ancillary goals that you hope to achieve by making the gift and meet with your advisors regarding the best structure for the gift.

Royce Lanning

Phone: 281-367-1222

Fax: 281-210-1361

__________________________________

[1] In summary, an asset given during life continues to be subject to the same or similar capital gains taxes as it was in the hands of the donor while an asset that is given after the donor’s death could be sold on that same date and not be subject to any capital gains tax.

Contact a Dedicated Texas Business Lawyer To Schedule a Consultation

Call 281-367-1222 or contact us online to schedule a meeting.

Recent Blog Posts

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

By The Strong Firm P.C. / March 13, 2024

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

As trusted legal advisors, we understand the complexities and challenges that employers face when navigating the landscape of employment law. With the ever-evolving regulatory environment, it's crucial for employers to stay informed and proactive in addressing legal concerns.

One

Read More

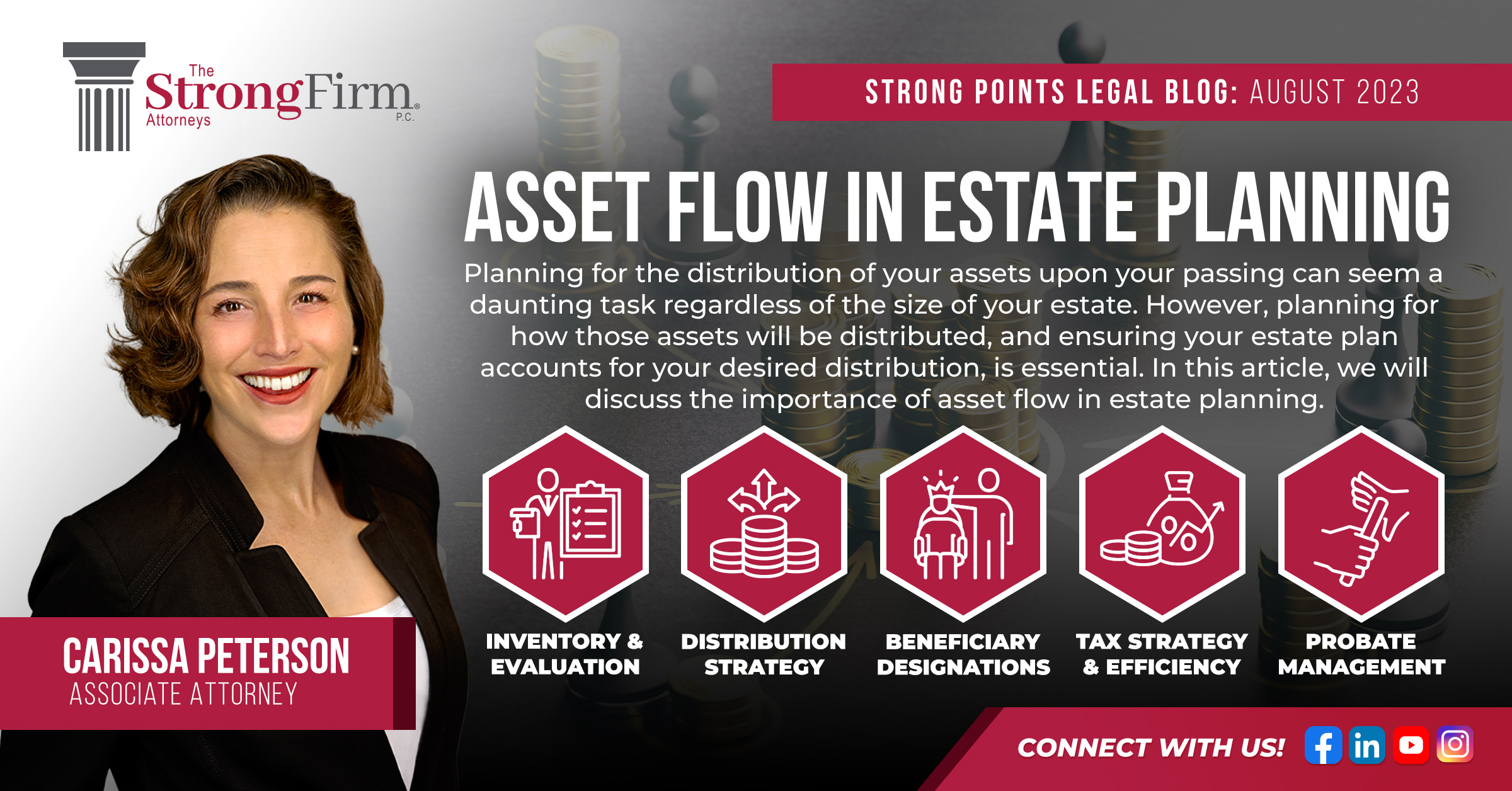

Asset Flow in Estate Planning

By Carissa Peterson / August 21, 2023

Planning for the distribution of your assets upon your passing can seem a daunting task regardless of the size of your estate. However, planning for how those assets will be distributed, and ensuring your estate plan accounts for your desired distribution, is essential. In this article, we will discuss the

Read More

Kelly Sullivan Joins The Strong Firm P.C. As Senior Counsel

By Bret L. Strong / June 10, 2022

The Strong Firm P.C. is excited to announce the addition of Kelly Sullivan to its team of experienced attorneys. Kelly adds exceptional strength to the firm’s established practice areas based on her wealth of experience in the areas of Litigation, Labor and Employment Law, Business Law and Governmental Law, Zoning

Read More

The Future of Non-Compete Agreements: Executive Order on Promoting Competition in the American Agreement

By Kristina Frankel / April 22, 2022

In July 2021, President Biden signed an Executive Order aiming to limit the use of restrictive covenants in employment relationships. Opening with the premise that “a fair, open, and competitive marketplace has long been a cornerstone of the American economy, while excessive market concentration threatens basic economic liberties, democratic accountability,

Read More

-

Video Vault

Watch videos done by our legal team to gain a better understanding of your legal needs. Our lawyers give video insight into areas such as Real Estate, Business Law, Mergers & Acquisitions and much more.![]()

Contact us