Search Site

1790 Hughes Landing Boulevard, Suite 200 | The Woodlands, Texas 77380

*Commitment Free Inquiry

281-367-1222

Four Ways to Fund your Business Succession Plan

An important part to a business succession plan is considering how to fund your succession plan. After all, the most intricate and thoroughly considered succession plan will fail if it lacks the funds necessary it execute the plan. The method of planning will depend on a multitude of factors but ideally a business owner will pick a funding mechanism that will take advantage of current business strengths in order to (a) compensate for expected weaknesses that arise during the transfer and/or (b) utilize current provisions under the law (e.g. tax code) to create an advantage for the business.

Business owners use a variety of funding technics to navigate these issues, such as:

- Cash Sinking Fund: Stated colloquially simply, this method could be called “saving for a rainy day.” In essence, this method of funding involves the process of setting aside funds on a regular basis in order to build up the cash reserves necessary to carry the company through the succession plan. An issue that arises with this type of financing is the failure to fund. For instance, the business (or owners) may fail to put aside sufficient funds or the funds may be needed sooner than expected.

- Installment Payments: This is essentially seller financing. Under this plan the owner that is selling their interest in the company (or that owner’s estate in the case of death) agrees to accept payments from the purchaser over time. A natural consequence of stretching payments over time is that it may cause liquidity issues for the seller early on when the need for cash is usually the greatest.

- 3rd Party Lender: Some succession plans address the liquidity issues arising from installment plans by utilizing third-party financing. 3rd Party financing will allow the buyer to provide the seller with an immediate influx of cash while still deferring the seller’s payments over time. An issue that can arise with 3rd party financing is finding a willing lender. This difficulty usually presents itself when the lender determines that it is being asked to lend funds for the purchase of a company that is vulnerable (e.g. if the company is losing an owner that contributed to the company’s past success).

- Insurance: Insurance products can be utilized to allow the business to fund business succession through the payment of premiums now for a source of liquid funding later. An issue that arises with insurance funding is that it requires careful consideration to obtain the right policy from the right insurer and can, in some cases, involve some significant “tax traps” depending on the structure of your succession plan.

Each funding method has strengths and weaknesses. No funding mechanism is correct for every business or every succession plan. Accordingly, it is important to identify your goals and discuss them with your planning professional.

Contact a Dedicated Texas Business Lawyer To Schedule a Consultation

Call 281-367-1222 or contact us online to schedule a meeting.

Recent Blog Posts

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

By The Strong Firm P.C. / March 13, 2024

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

As trusted legal advisors, we understand the complexities and challenges that employers face when navigating the landscape of employment law. With the ever-evolving regulatory environment, it's crucial for employers to stay informed and proactive in addressing legal concerns.

One

Read More

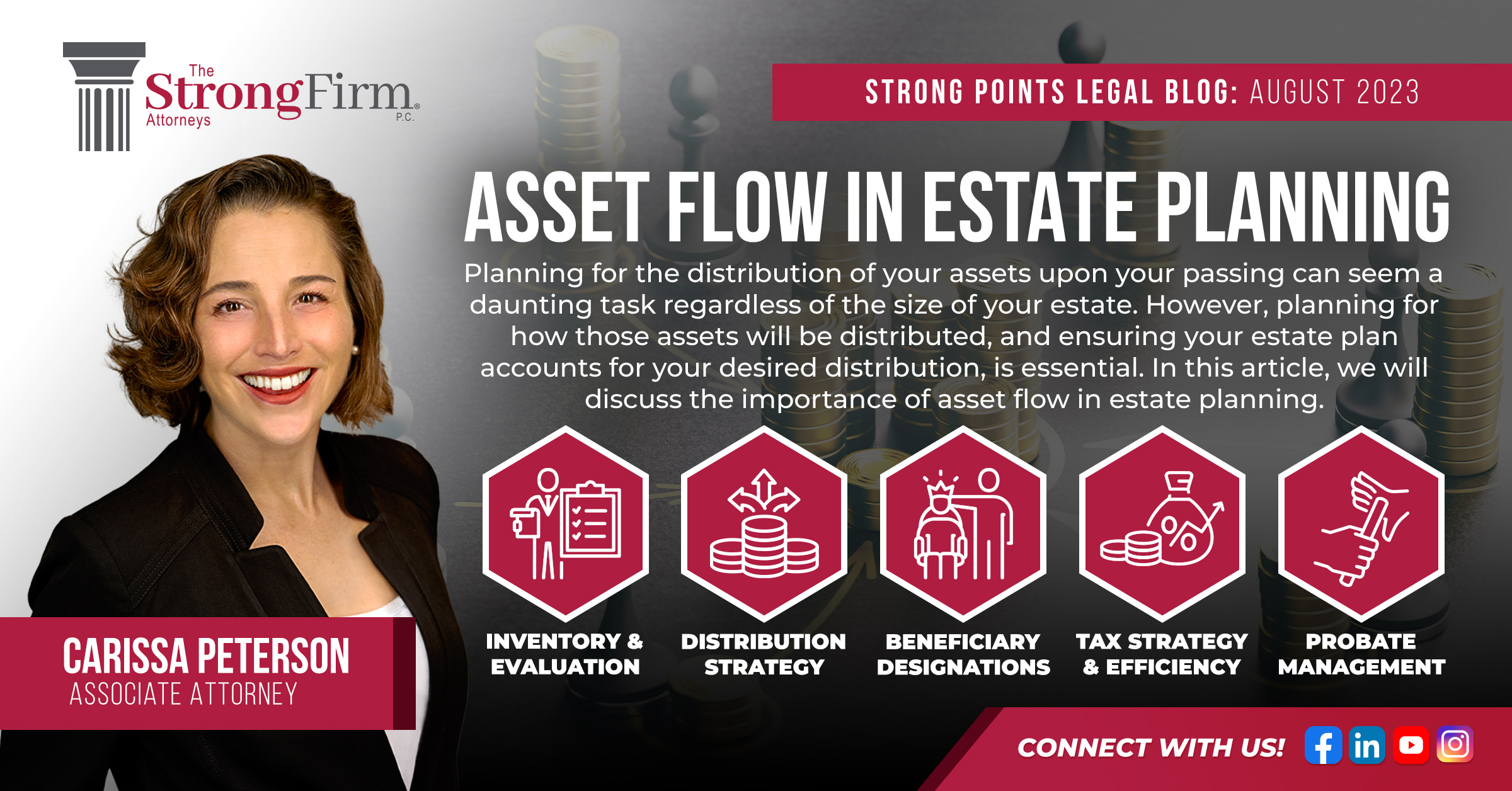

Asset Flow in Estate Planning

By Carissa Peterson / August 21, 2023

Planning for the distribution of your assets upon your passing can seem a daunting task regardless of the size of your estate. However, planning for how those assets will be distributed, and ensuring your estate plan accounts for your desired distribution, is essential. In this article, we will discuss the

Read More

Kelly Sullivan Joins The Strong Firm P.C. As Senior Counsel

By Bret L. Strong / June 10, 2022

The Strong Firm P.C. is excited to announce the addition of Kelly Sullivan to its team of experienced attorneys. Kelly adds exceptional strength to the firm’s established practice areas based on her wealth of experience in the areas of Litigation, Labor and Employment Law, Business Law and Governmental Law, Zoning

Read More

The Future of Non-Compete Agreements: Executive Order on Promoting Competition in the American Agreement

By Kristina Frankel / April 22, 2022

In July 2021, President Biden signed an Executive Order aiming to limit the use of restrictive covenants in employment relationships. Opening with the premise that “a fair, open, and competitive marketplace has long been a cornerstone of the American economy, while excessive market concentration threatens basic economic liberties, democratic accountability,

Read More

-

Video Vault

Watch videos done by our legal team to gain a better understanding of your legal needs. Our lawyers give video insight into areas such as Real Estate, Business Law, Mergers & Acquisitions and much more.![]()

Contact us