Search Site

1790 Hughes Landing Boulevard, Suite 200 | The Woodlands, Texas 77380

*Commitment Free Inquiry

281-367-1222

Any parent with a special needs child understands that the hardships their children face are much more than their physical disability. They also understand that the words “special needs” is one of the broadest categories in our language. “Special needs” is the same term to identify a child with muscular dystrophy who may never be able to provide for themselves and a child on the autism spectrum who will graduate college, have a successful career and a family. Historically, our country’s main benefit program for special needs children, Supplemental Security Income (SSI), disincentivized any special needs adult from becoming financially independent. SSI is means-tested, meaning there is an asset limit of $2,000 at all times. Picture the sweet man with down syndrome who is bagging your groceries at Whole Foods. He works hard every day to earn his paycheck. In the past, our laws have taught him, that because he was special, he could not save any of his money like other adults, but he must spend most of every paycheck in order to stay qualified for his benefits. Thankfully, this is no longer the case.

In 2014, The Achieving A Better Life Experience (ABLE) Act was created by the Obama Administration. The ABLE Act added section 529A to the Internal Revenue Code, which created a new savings option for eligible individuals with disabilities to save money in a tax-advantaged account, to be used for qualified expenses, and keep their eligibility for government benefits. In May 2018, the Texas Comptroller opened enrollment in the Texas ABLE Program. The program is open to eligible Texans who experience the onset of a disability before the age of 26 and are entitled to SSI or SSDI benefits, have a condition on the Social Security Administration’s list of Compassionate Allowances Conditions (https://www.ssa.gov/compassionateallowances/ conditions.htm), or a physician’s diagnosis of a qualifying condition. An ABLE account holder and their family can contribute an annual total of up to $15,000 per year to an ABLE Account. An account can hold as much as $100,000 at any one time without affecting eligibility for Supplemental Security Income (SSI). Savings and investments grow tax-free. Withdrawals for qualified disability expenses are tax-free. Qualified disability expenses include expenses related to housing, education, transportation, employment training and support, assistive technology and personal support services, health, prevention and wellness, financial management and administrative services, legal fees, and expenses for oversight and monitoring, funeral and burial expenses.

In 2015, Congress removed the requirement that are only able to open an ABLE account in your state of residency. The Able National Resource Center (www.ablenrc.org) maintains information on each state’s program. It is a good idea to compare each state, because ABLE account fees and investment options vary by state. Some states manage their own ABLE program, some state contacted with other state to manage their ABLE program, and some states have contracted with private companies to manage their ABLE program. For example, the state of Massachusetts contacted with Fidelity Investments, who has created The Attainable Saving Plan (https://www.fidelity.com/able/attainable/overview).

In the special needs community, knowledge on every opportunity for benefits can completely change quality of life. If you have any questions or concerns on ABLE accounts, contact a local elder attorney or ask your financial advisor if they have any additional information on ABLE accounts.

Contact a Dedicated Texas Business Lawyer To Schedule a Consultation

Call 281-367-1222 or contact us online to schedule a meeting.

Recent Blog Posts

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

By The Strong Firm P.C. / March 13, 2024

Navigating Employment Law Concerns: A Guide To The Biggest Risks for Texas Employers

As trusted legal advisors, we understand the complexities and challenges that employers face when navigating the landscape of employment law. With the ever-evolving regulatory environment, it's crucial for employers to stay informed and proactive in addressing legal concerns.

One

Read More

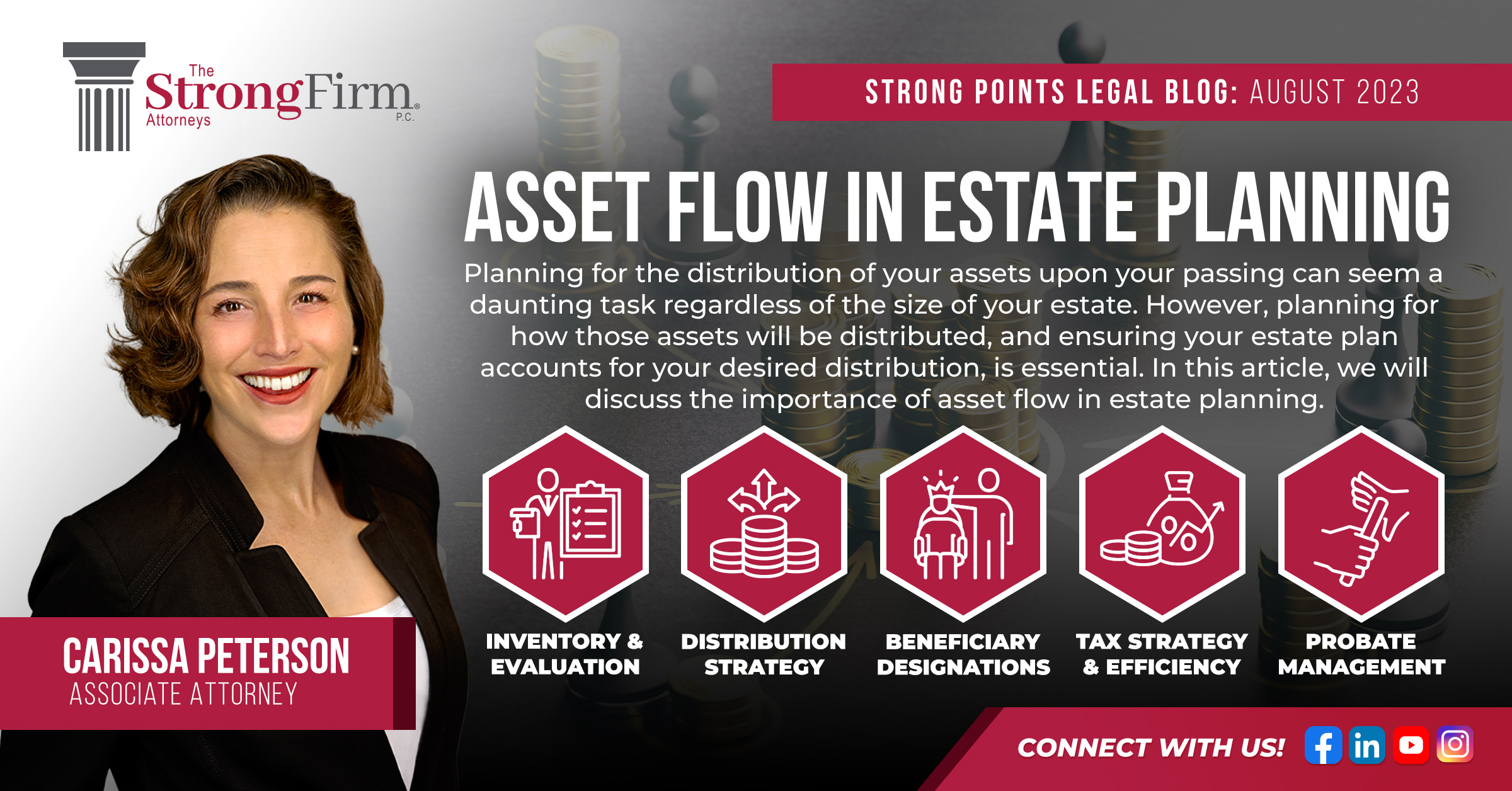

Asset Flow in Estate Planning

By Carissa Peterson / August 21, 2023

Planning for the distribution of your assets upon your passing can seem a daunting task regardless of the size of your estate. However, planning for how those assets will be distributed, and ensuring your estate plan accounts for your desired distribution, is essential. In this article, we will discuss the

Read More

Kelly Sullivan Joins The Strong Firm P.C. As Senior Counsel

By Bret L. Strong / June 10, 2022

The Strong Firm P.C. is excited to announce the addition of Kelly Sullivan to its team of experienced attorneys. Kelly adds exceptional strength to the firm’s established practice areas based on her wealth of experience in the areas of Litigation, Labor and Employment Law, Business Law and Governmental Law, Zoning

Read More

The Future of Non-Compete Agreements: Executive Order on Promoting Competition in the American Agreement

By Kristina Frankel / April 22, 2022

In July 2021, President Biden signed an Executive Order aiming to limit the use of restrictive covenants in employment relationships. Opening with the premise that “a fair, open, and competitive marketplace has long been a cornerstone of the American economy, while excessive market concentration threatens basic economic liberties, democratic accountability,

Read More

-

Video Vault

Watch videos done by our legal team to gain a better understanding of your legal needs. Our lawyers give video insight into areas such as Real Estate, Business Law, Mergers & Acquisitions and much more.![]()

Contact us